6.2.1.3. Regularized Regression#

When a linear model has many features - especially when they are correlated or only weakly relevant - Ordinary Least Squares tends to overfit: it assigns large, noisy coefficients to chase training-set variation that does not generalise.

Regularization fixes this by adding a penalty on the magnitude of the coefficients directly to the loss function. The optimiser is now forced to balance fitting the data and keeping the coefficients small. The result is a model that is slightly biased but has much lower variance, and usually generalises much better.

There are three main variants:

Variant |

Penalty |

Key behaviour |

|---|---|---|

Ridge (L2) |

Sum of squared coefficients |

Shrinks all coefficients toward zero uniformly; none become exactly zero |

Lasso (L1) |

Sum of absolute coefficients |

Drives some coefficients to exactly zero - automatic feature selection |

Elastic Net |

Weighted L1 + L2 |

Combines both: sparse like Lasso, stable with correlated features like Ridge |

The Math#

All three regularized models minimise the same base MSE loss (as in Linear Regression), plus a penalty term controlled by the hyperparameter \(\alpha\).

Ridge (L2)#

The L2 penalty creates a smooth penalty landscape - no direction is treated differently, so all coefficients shrink together. The solution remains unique even when features are correlated.

Lasso (L1)#

The L1 penalty has sharp corners at zero in each dimension. This geometric property means the optimum frequently lands exactly on zero for some coefficients, producing sparse solutions.

Elastic Net#

l1_ratio \(\rho = 1\) recovers Lasso; \(\rho = 0\) recovers Ridge. A value like \(0.5\) gives an equal blend.

In scikit-learn#

from sklearn.linear_model import Ridge, Lasso, ElasticNet

ridge = Ridge(alpha=1.0)

lasso = Lasso(alpha=0.5, max_iter=5000)

enet = ElasticNet(alpha=0.5, l1_ratio=0.5, max_iter=5000)

Key hyperparameters:

alpha- regularization strength; higher → stronger shrinkage (useRidgeCV/LassoCVto tune)l1_ratio(Elastic Net only) - blend between L1 and L2

Example#

ridge = Ridge(alpha=1.0)

lasso = Lasso(alpha=0.5, max_iter=5000)

enet = ElasticNet(alpha=0.5, l1_ratio=0.5, max_iter=5000)

ridge_r2, ridge_rmse = test_stats(ridge)

lasso_r2, lasso_rmse = test_stats(lasso)

enet_r2, enet_rmse = test_stats(enet)

pd.DataFrame({

"Model": ["Ridge (α=1.0)", "Lasso (α=0.5)", "Elastic Net (α=0.5, ρ=0.5)"],

"Test R²": [ridge_r2, lasso_r2, enet_r2],

"Test RMSE": [ridge_rmse, lasso_rmse, enet_rmse],

})

| Model | Test R² | Test RMSE | |

|---|---|---|---|

| 0 | Ridge (α=1.0) | 0.978 | 26.3 |

| 1 | Lasso (α=0.5) | 0.978 | 26.6 |

| 2 | Elastic Net (α=0.5, ρ=0.5) | 0.924 | 49.1 |

Ridge achieves \(R^2\) = 0.978, Lasso 0.978, and Elastic Net 0.924. The dataset has only 6 informative features out of 10, so Lasso’s feature-selection behaviour is particularly relevant here.

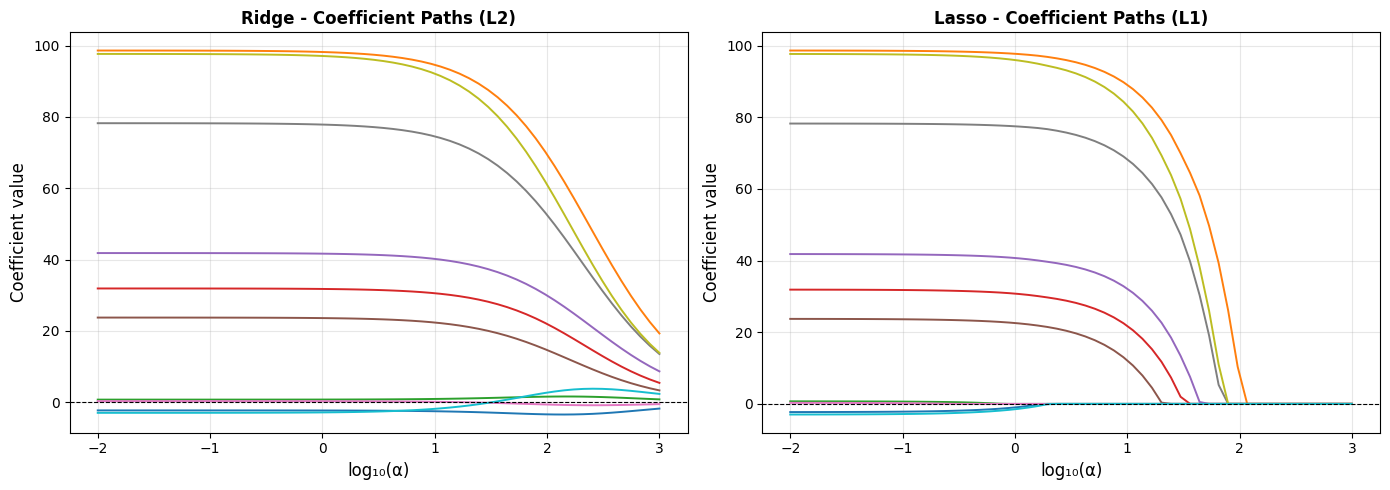

Coefficient Paths - How \(\alpha\) Changes the Solution#

As \(\alpha\) increases, more regularization is applied and all coefficients shrink. For Lasso, they hit zero one by one:

In the Ridge plot, every line smoothly approaches zero but never fully reaches it. In the Lasso plot, lines hit zero and stay there - those are features being excluded from the model entirely.

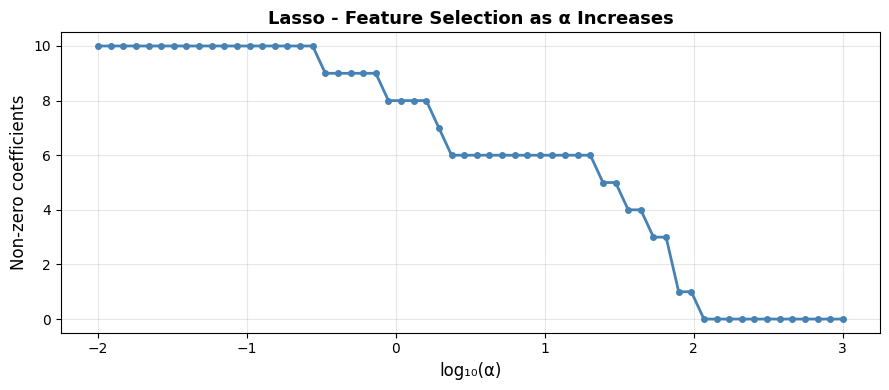

How Many Features Does Lasso Keep?#

non_zero_by_alpha = [(np.sum(lasso_coefs[i] != 0)) for i in range(len(alphas))]

plt.figure(figsize=(9, 4))

plt.plot(np.log10(alphas), non_zero_by_alpha, "o-", markersize=4, linewidth=2, color="steelblue")

plt.xlabel("log₁₀(α)", fontsize=12)

plt.ylabel("Non-zero coefficients", fontsize=12)

plt.title("Lasso - Feature Selection as α Increases", fontsize=13, fontweight="bold")

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# Count non-zero coefficients in the fitted Lasso (α=0.5)

n_selected = int(np.sum(lasso.coef_ != 0))

glue("lasso-n-selected", n_selected, display=False)

With \(\alpha = 0.5\), Lasso retains 9 of the 10 features, correctly discarding most of the non-informative ones.

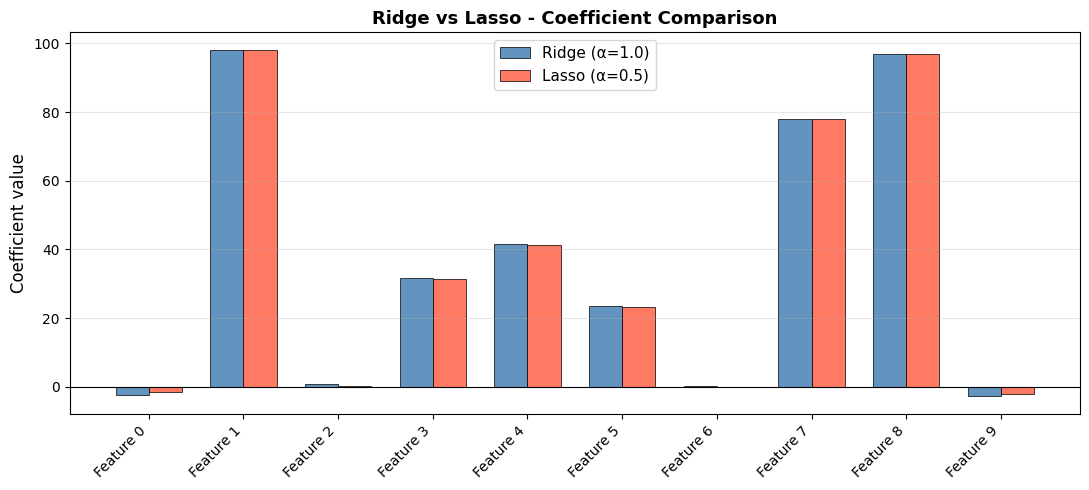

Ridge vs Lasso - Side-by-Side Coefficient Comparison#

Choosing Between Ridge, Lasso, and Elastic Net#

Situation |

Recommended |

|---|---|

Many features, each contributes a little |

Ridge - keeps all features, stable |

Few features truly matter (sparse signal) |

Lasso - zeroes out irrelevant features |

Correlated features + you want sparsity |

Elastic Net - handles correlations better than pure Lasso |

Unsure |

Elastic Net - safe default that interpolates between both |

Tip

Use RidgeCV, LassoCV, or ElasticNetCV to automatically select alpha via cross-validation instead of guessing.